TV advertising 2012-2017

Over the next five years, a CAGR of 5.3% will see the TV advertising sector pass the US$200bn revenue mark, with global revenues valued at US$209.4bn in 2017 compared with US$162.1bn in 2012.

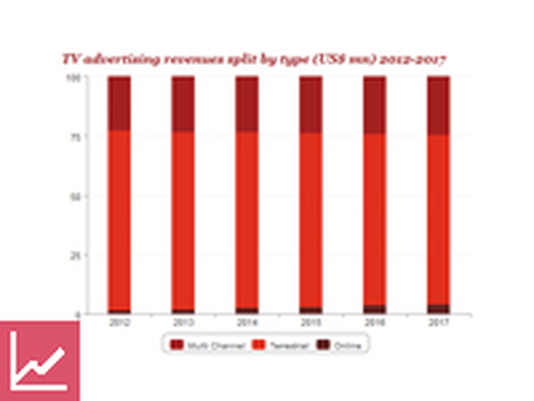

The ability of legacy terrestrial TV networks to deliver the mass audiences so attractive to advertisers will ensure that the terrestrial sector continues to dominate TV advertising globally, with 73% of net revenues (US$118bn) attributable to free-to-air terrestrial channels in 2012. That figure will increase to US$146bn by 2017, representing a slightly lower proportion of the total, at 70%. That drop in percentage will be driven by the move to digital broadcasting, which facilitates the rise of pay and thematic channels, and increasing broadband penetration means there will be greater usage of online video services, including catch-up services from traditional broadcasters.

TV advertising revenues split by type (US$ mn) 2012-2017

Over the next five years, the TV advertising sector will pass US$200bn in revenue—with a CAGR of 5.3%—with global revenues valued at US$209.4bn in 2017 compared with US$162.1bn in 2012. Despite a rise in pay TV subscriptions, terrestrial television will account for 69.6% of all TV advertising revenues in 2017.

Over the next five years, a CAGR of 5.3% will see the TV advertising sector pass the US$200bn revenue mark, with global revenues valued at US$209.4bn in 2017 compared with US$162.1bn in 2012.

The ability of legacy terrestrial TV networks to deliver the mass audiences so attractive to advertisers will ensure that the terrestrial sector continues to dominate TV advertising globally, with 73% of net revenues (US$118bn) attributable to free-to-air terrestrial channels in 2012. That figure will increase to US$146bn by 2017, representing a slightly lower proportion of the total, at 70%. That drop in percentage will be driven by the move to digital broadcasting, which facilitates the rise of pay and thematic channels, and increasing broadband penetration means there will be greater usage of online video services, including catch-up services from traditional broadcasters.

TV advertising revenues split by type (US$ mn) 2012-2017

Over the next five years, the TV advertising sector will pass US$200bn in revenue—with a CAGR of 5.3%—with global revenues valued at US$209.4bn in 2017 compared with US$162.1bn in 2012. Despite a rise in pay TV subscriptions, terrestrial television will account for 69.6% of all TV advertising revenues in 2017.

The US will still dominate global TV advertising revenues, accounting for 39.0% of the global total in 2017, which is only a modest drop from 2012’s 39.4%. But the fastest rates of growth will be in other markets, including Kenya (16% CAGR), Indonesia (15% CAGR), India (12% CAGR), Nigeria (11% CAGR) and Brazil (10% CAGR).

The 5 fastest growing TV advertising markets; 2013-17 CAGR (%)

Online TV advertising revenues will treble from 2012 to 2017 but will remain a fraction of traditional TV revenues. In Japan and South Korea, online TV advertising will, on average, more than double every year until 2017. Such aggressive growth will see Japan become the third-largest market for online TV advertising globally, behind only the US and the UK. South Korea’s emergence will move it up to number eight.

The 5 fastest growing TV advertising markets; 2013-17 CAGR (%)

Online TV advertising revenues will treble from 2012 to 2017 but will remain a fraction of traditional TV revenues. In Japan and South Korea, online TV advertising will, on average, more than double every year until 2017. Such aggressive growth will see Japan become the third-largest market for online TV advertising globally, behind only the US and the UK. South Korea’s emergence will move it up to number eight.