Internet access

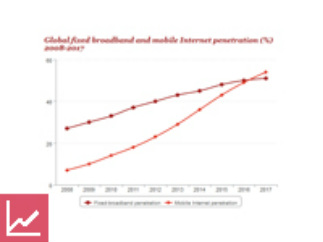

Despite their being worth US$393bn, Internet access services still had plenty of growth left in the global market at the end of 2012: globally, just 40% of households were subscribed to fixed broadband, and less than one in four people had mobile Internet access.

Global spend on Internet access services will increase at an impressive, 11% CAGR over the next five years to reach over US$665bn in 2017. Mobile Internet revenues will drive much of the growth, overtaking those from fixed broadband in 2014 to account for 58% of overall Internet access spend at the end of the forecast period.

Global fixed broadband and mobile Internet penetration (%) 2008-2017

After years of home broadband being the most popular way to access the Internet, a fundamentally different form will come to dominate: access via mobile broadband, most often via mobile phones rather than PCs and laptops. Penetration of mobile-Internet services will reach 54% by year-end 2017 compared with 51% for fixed broadband.

Despite their being worth US$393bn, Internet access services still had plenty of growth left in the global market at the end of 2012: globally, just 40% of households were subscribed to fixed broadband, and less than one in four people had mobile Internet access.

Global spend on Internet access services will increase at an impressive, 11% CAGR over the next five years to reach over US$665bn in 2017. Mobile Internet revenues will drive much of the growth, overtaking those from fixed broadband in 2014 to account for 58% of overall Internet access spend at the end of the forecast period.

Global fixed broadband and mobile Internet penetration (%) 2008-2017

After years of home broadband being the most popular way to access the Internet, a fundamentally different form will come to dominate: access via mobile broadband, most often via mobile phones rather than PCs and laptops. Penetration of mobile-Internet services will reach 54% by year-end 2017 compared with 51% for fixed broadband.

The US is the largest territory in fixed broadband, with high penetration and high average revenue per user (ARPU). After exceeding the revenues of Japan in 2012, China is closing the gap on the US due to its aggressive double digit growth in subscribers despite considerably lower ARPU.

US, China and Japan fixed broadband access revenues (US$ mn) 2011-2017

Mobile Internet revenues, worth US$259bn in 2014, will account for more than 50% of total Internet access spend, overtaking those from fixed broadband. By 2017, mobile Internet revenues will exceed US$385bn and account for 58% of total Internet access spend.

Internet access revenues split by fixed broadband and mobile internet (US$ mn) 2008-2017

Growth will increasingly be driven by emerging markets. Brazil, China, India and Russia alone will account for 45% of fixed-broadband subscriptions and 50% of mobile Internet users by the end of 2017.

BRIC countries share of mobile Internet subscribers (%) 2012 & 2017

US, China and Japan fixed broadband access revenues (US$ mn) 2011-2017

Mobile Internet revenues, worth US$259bn in 2014, will account for more than 50% of total Internet access spend, overtaking those from fixed broadband. By 2017, mobile Internet revenues will exceed US$385bn and account for 58% of total Internet access spend.

Internet access revenues split by fixed broadband and mobile internet (US$ mn) 2008-2017

Growth will increasingly be driven by emerging markets. Brazil, China, India and Russia alone will account for 45% of fixed-broadband subscriptions and 50% of mobile Internet users by the end of 2017.

BRIC countries share of mobile Internet subscribers (%) 2012 & 2017