Internet advertising

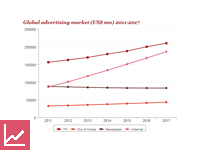

On a global level, Internet advertising continues to defy the world’s wider economic problems, growing in terms of both volume and its share of the global advertising pie. Internet advertising reached US$100.2bn in 2012, representing year-on-year growth of 17% and a 20% share of the global advertising market. Fuelled largely by substantial growth of the market in the developing world—although many of the developed markets will continue to see growth too—the market will reach US$185.4bn in 2017, a growth rate of 13% over the five-year forecast period. By that point, Internet advertising will take a 29% share of the total global ad market, making it the world’s second-largest advertising medium.

Global advertising market (US$ mn) 2011-2017

Set to be worth more than US$185bn in 2017, Internet advertising will constitute 29% of the world’s total advertising market, making it the world’s second-largest medium for advertising, after TV.

On a global level, Internet advertising continues to defy the world’s wider economic problems, growing in terms of both volume and its share of the global advertising pie. Internet advertising reached US$100.2bn in 2012, representing year-on-year growth of 17% and a 20% share of the global advertising market. Fuelled largely by substantial growth of the market in the developing world—although many of the developed markets will continue to see growth too—the market will reach US$185.4bn in 2017, a growth rate of 13% over the five-year forecast period. By that point, Internet advertising will take a 29% share of the total global ad market, making it the world’s second-largest advertising medium.

Global advertising market (US$ mn) 2011-2017

Set to be worth more than US$185bn in 2017, Internet advertising will constitute 29% of the world’s total advertising market, making it the world’s second-largest medium for advertising, after TV.

Search remains the dominant form of online advertising globally, despite that its share dropped by two percentage points to 41% in 2017 (moving increasingly towards mobile and video advertising). Where Google is not the market leader—such as in Japan and South Korea—search tends not to be the dominant online advertising format.

Search revenues (US$ mn) and as a % of total revenues 2008-2017

The display market is set to grow at a CAGR of 10% over the forecast period, reaching US$49.9bn in 2017. Advertisers will have to consider new ways they can best use display advertising.

Display revenues (US$ mn) and as a % of total revenues 2008-2017

Classifieds will grow at a CAGR of 7%, reaching US$20.2bn in 2017. Online classifieds are set to take over from their print equivalents in developing economies in the next five years. However, this segment’s share of the total online ad market will be lower in 2017 than in 2012.

Classified revenues (US$ mn) and as a % of total revenues 2008-2017

The online video-advertising market boomed in 2012, with an increase in annual revenue of approximately US$1bn, representing year-on-year growth of 33%. That growth is set to continue over the forecast period, with revenues reaching US$12bn in 2017, boosted by a 26% CAGR.

Video revenues (US$ mn) and as a % of total revenues 2008-2017

Search revenues (US$ mn) and as a % of total revenues 2008-2017

The display market is set to grow at a CAGR of 10% over the forecast period, reaching US$49.9bn in 2017. Advertisers will have to consider new ways they can best use display advertising.

Display revenues (US$ mn) and as a % of total revenues 2008-2017

Classifieds will grow at a CAGR of 7%, reaching US$20.2bn in 2017. Online classifieds are set to take over from their print equivalents in developing economies in the next five years. However, this segment’s share of the total online ad market will be lower in 2017 than in 2012.

Classified revenues (US$ mn) and as a % of total revenues 2008-2017

The online video-advertising market boomed in 2012, with an increase in annual revenue of approximately US$1bn, representing year-on-year growth of 33%. That growth is set to continue over the forecast period, with revenues reaching US$12bn in 2017, boosted by a 26% CAGR.

Video revenues (US$ mn) and as a % of total revenues 2008-2017

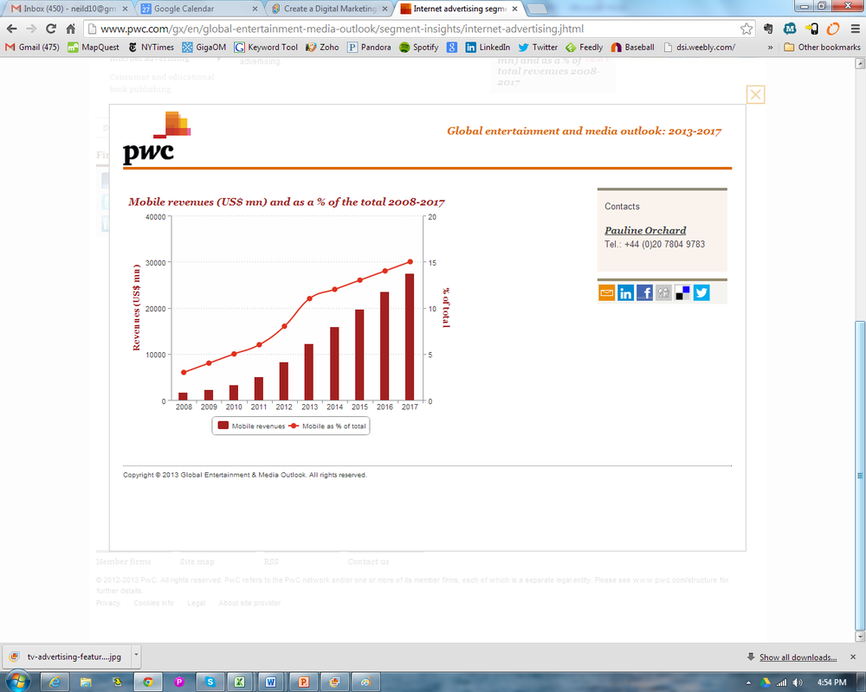

Mobile advertising is finally set to take off properly, with growth forecast across all regions over the next five years: a 27% CAGR will ensure mobile advertising revenues will be in excess of US$27bn in 2017, constituting 15% of Internet advertising revenues.

Mobile revenues (US$ mn) and as a % of total revenues 2008-2017

Mobile revenues (US$ mn) and as a % of total revenues 2008-2017

How we define this segment

This segment is split as spending by advertisers either through a fixed-line connection or via mobile devices. The fixed-line categories consist of advertising via paid search, display, classified and video advertising. Display includes all banner, rich media, sponsorship, lead generation and e-mail related advertising. The mobile category includes all advertising delivered direct to mobile devices via formats designed for the specific device.

To maintain consistency across all segments, the advertising revenues are shown as net revenues which exclude agency commissions and production costs where applicable.

The Internet advertising segment also includes online television, digital newspaper and magazine advertising, digital directory advertising and online radio. These are also included in their respective segments but are eliminated at total advertising level to avoid any double counting.

What data is included in the online Outlook?

Forecasts for advertising spend in the Internet advertising segment across 50 countries cover (where available):

· Total Internet advertising (US$ m)

· Paid search Internet advertising (US$ m)

· Display Internet advertising (US$ m)

· Classified Internet advertising (US$ m)

· Video Internet advertising (US$ m)

· Mobile Internet advertising (US$ m)

· Total wired Internet advertising (US$ m) (total = search + display + classified + video)

This segment is split as spending by advertisers either through a fixed-line connection or via mobile devices. The fixed-line categories consist of advertising via paid search, display, classified and video advertising. Display includes all banner, rich media, sponsorship, lead generation and e-mail related advertising. The mobile category includes all advertising delivered direct to mobile devices via formats designed for the specific device.

To maintain consistency across all segments, the advertising revenues are shown as net revenues which exclude agency commissions and production costs where applicable.

The Internet advertising segment also includes online television, digital newspaper and magazine advertising, digital directory advertising and online radio. These are also included in their respective segments but are eliminated at total advertising level to avoid any double counting.

What data is included in the online Outlook?

Forecasts for advertising spend in the Internet advertising segment across 50 countries cover (where available):

· Total Internet advertising (US$ m)

· Paid search Internet advertising (US$ m)

· Display Internet advertising (US$ m)

· Classified Internet advertising (US$ m)

· Video Internet advertising (US$ m)

· Mobile Internet advertising (US$ m)

· Total wired Internet advertising (US$ m) (total = search + display + classified + video)